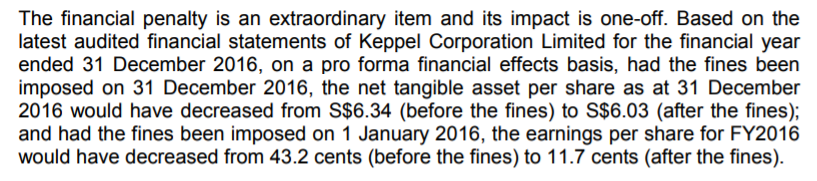

Keppel Corp has issued an announcement, dated 23 Dec 2017.

Among other things, it highlighted the impact to its pro-forma NTA; EPS;

You can read its full announcement here

News agencies expect shares price of KCL likely to have immediate knee jerk reaction when market opens on Tuesday.

As revealed in its latest financial statement, KCL has survived as a group with almost non-reliance on its O&M segment for earning.

(see its 9M17 net earning I extracted it below:)

In contrast, KOM’s revenue still constitutes a substantial 30% to the conglomerate. Further diversification is therefore imminent to correct such asymmetrical earning structure.

To be sure, it is a non-trivial mammoth task to consider getting rid of such heavy-weight oil rig business asset. The persistently low oil price coupled with the lack of E&P CapEx up-stream, exacerbate the process even if the board has decided to divest bulk of the O&M sector through strategic review.

Fast forward to 2021, the situation of oil-oversupply may improve. But for now, companies in the O&M sector still have to grapple with uncertainties, in an attempt to maximise their shareholders value.

written by George Seah Singapore

佘文发硕士

(for my blog)

P.S. statements attached above are extracted verbatim from relevant company’s public announcement or presentation materials.

{kind=link}

You must be logged in to post a comment.